Eight times a year, thousands of economists, analysts, and money managers tune in as the Federal Open Market Committee releases a statement about their policy decision. We’ve all heard the age old adage ‘Don’t fight the Fed,’ but does Fed day really matter? I decided to take a look.

For this study, I define ‘matter’ as resulting in a peak or trough in prices over a predetermined time period. Put simply, I look for a well-defined change in the trend.

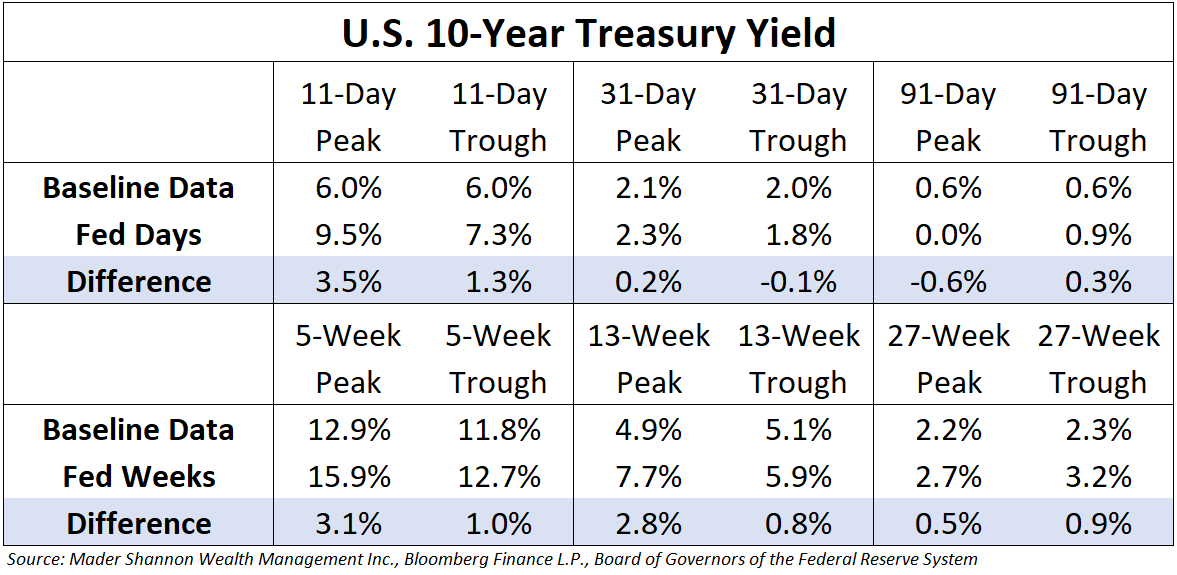

On any given day, the odds that the price of the S&P 500 Index is higher than both the preceding 5 days and the 5 days to follow (a peak) is 5.9%. The odds that a day’s closing price will be the low of the total 11-day period (a trough) is 6.0%. Thus, the odds that any day of trading marks a definitive peak or trough is 11.9% (6.0% + 5.9%). We can use the same logic, with different time intervals, to identify more significant turning points. The table below summarizes my findings for the S&P 500 and the U.S. 10-Year Treasury Yield.

So what happens when we overlay FOMC decision dates? I pulled every meeting and decision date since 1993 and compared it to our baseline data. Let’s look at equities first.

Fed days are about 1.5% more likely to change the trend over an 11-day period, 2.5% more likely over a 31-day period, and have virtually no bearing over a 3 month period. On a weekly basis, decision week is 3.3% more likely to occur while equities are setting 5-week highs, but have less bearing over longer time frames.

The impact on Treasuries is somewhat larger, especially on a weekly basis.

Notably, Fed decisions are more likely to result in yields topping over 11-day, 5-week, and 13-week periods.

The evidence clearly indicates that FOMC meetings do measurably increase the odds of market turning points, but what does a 4.8% (the maximum for any time period in this study) increase in the odds actually mean? It means for that time period over the last 25 years, 11 more meetings resulted in trend changes than what would be implied by the baseline – only one meeting every 2.27 years. Even when we choose the most favorable time period, there’s still a 95% chance that a Fed meeting won’t change the trend.

As someone who reads each FOMC press release and watches every press conference, that hurts. No one wants to feel like they’ve wasted their time. But I’m not yet so cynical to believe the Fed doesn’t matter at all. Given how actively Fed members work to manage expectations, perhaps this is really a tribute to their success in not surprising market participants (that hurts, too. The last thing I want is more Fed talk).

As we head towards another meeting this week, I know I’ll still read the release and watch Mr. Powell answer questions – the backdrop of monetary policy is a vital input to any top-down macro approach. That said, these findings definitely reduce the weight I’ll place on market activity around decisions. I’ll spend more time trying to identify the current trend and less trying to find something that will change it.

What do you think?

Nothing in this post or on this site is intended as a recommendation or an offer to buy or sell securities. Posts are meant for informational and entertainment purposes only. I or my affiliates may hold positions in securities mentioned in posts. Please see my Disclosure page for more information.